It was at the very beginning of the fourth year of medical school that we had our first child. So, we decided to get life insurance. I didn’t know who to turn to at first, but then I was directed to an insurance agent at a well-known mutual fund company who happened to be my friend’s brother. As I sat down, he asked if I was healthy. I replied that I was otherwise healthy outside of an essential tremor (diagnosed by a neurology resident as I aptly performed my first lumbar puncture with shaking hands in my third year of medical school) and a remote ADHD diagnosis.

He told me that I should apply for disability insurance despite the fact that — as a medical student — I had no income. I said no a few times before he talked me into it.

Long story short, my application was flat-out denied. No exclusion for my tremor was offered. The result was a flat denial, and it turns out this was a catastrophic financial mistake that should never happen to a physician-in-training.

The reason that this is important is that most hospitals with residency and fellowship programs offer “guaranteed” standard issue (GSI) disability insurance policies that forego medical underwriting. They never look into your medical history.

Typically, the only stipulations for these policies are that:

1) you can’t be currently disabled or previously disabled and

2) you cannot have been denied disability insurance previously.

That’s it.

Since I had been denied, I was no longer eligible for the GSI plan. The bridge had been burned. Thanks to my friend’s brother, I do not have personal disability insurance to this day and must rely on my group policy provided by my employer, which is inadequate as you’ll read below. Should I ever become disabled, my family will be in a potentially catastrophic financial situation. All because I didn’t understand how disability insurance worked while in training.

Why Group Disability Insurance Coverage is Inadequate

It is important to mention that both the GSI and fully underwritten disability insurance policies are Individual/Personal policies. These are different from the group policies offered to you by your employer or large medical organizations (e.g., the American Medical Association).

Individual policies are crucial to your asset protection because they are portable (i.e., they come with you if you change employers), while group policies are not (i.e., if you leave your employer or the organization that sponsored your group plan cancels, you are no longer protected). Group policies can also be canceled or changed at any point. You have no protection from this, whereas an individual policy like the GSI or a fully underwritten disability policy is non-cancelable and guaranteed renewal.

The definition of disability is also inadequate in many of the group policies provided by employers. This is why you need an individual policy (e.g., a GSI or fully underwritten policy). I recommend obtaining a GSI plan first as the safest course of action if you have any medical problems. However, you must know that a GSI policy is typically only available during training and for the 3-6 months after training. This is why every resident must go about getting disability insurance during training.

How to Go About Getting Disability Insurance

If my example above serves as how to not go about getting disability insurance, let’s answer the question, “When should you get an individual disability insurance policy?” The answer is the day before you get disabled. Since you and I do not know when that will be, the next best answer is as soon as you have an income. However, you must do it the right way to avoid getting denied like I did.

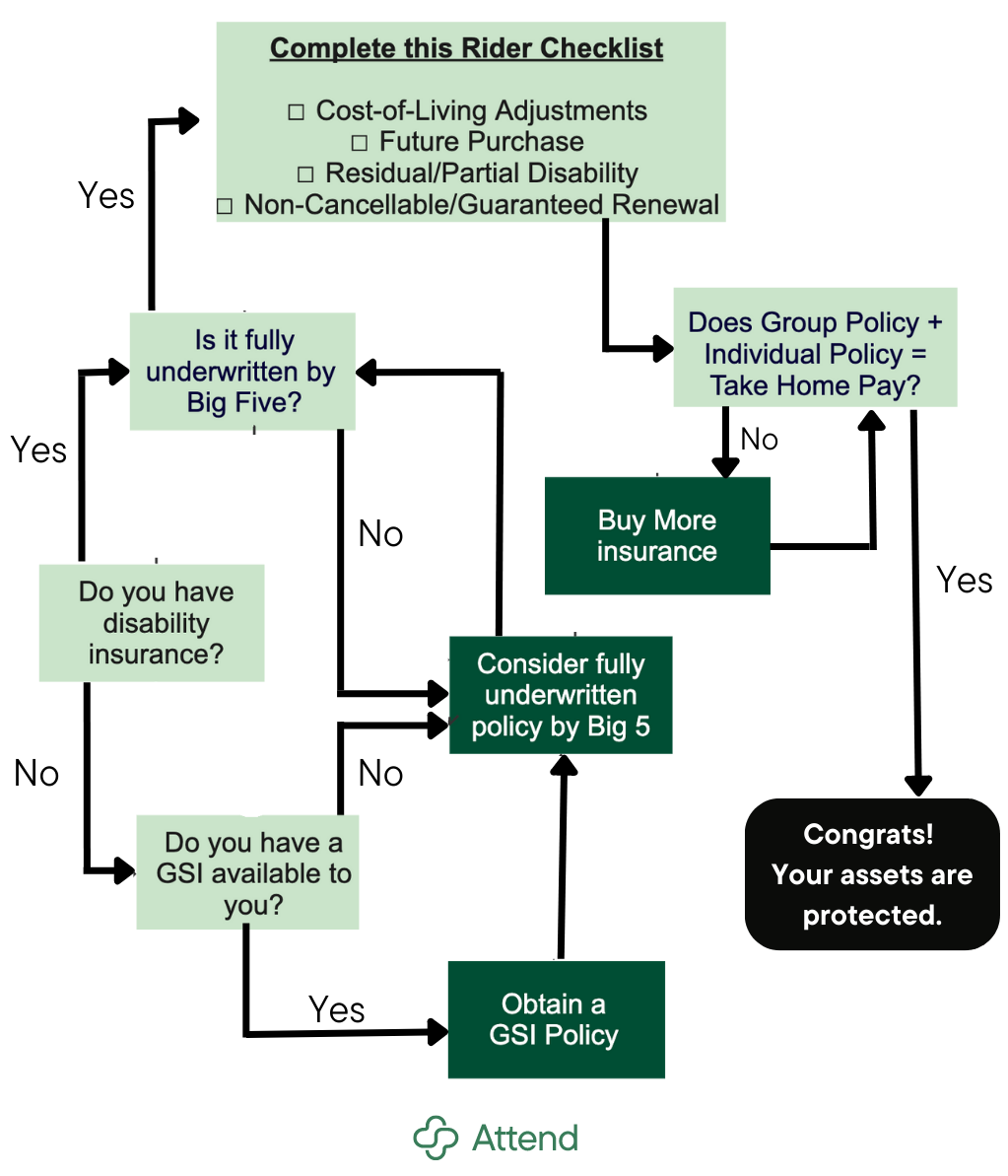

Here is the process I recommend that places you at the least risk of getting denied while getting the disability insurance you need. I've included a flowchart to walk through this process.

As I mentioned, if you are in training, there is a good chance you have a Guaranteed Standard Issue (GSI) policy available to you. However, the GSI is typically only available during training and for 3 to 6 months after you finish. So, don’t sleep on this. You should get disability insurance as soon as you have an income as a physician-in-training and fit it into your budget.

As I mentioned, if you are in training, there is a good chance you have a Guaranteed Standard Issue (GSI) policy available to you. However, the GSI is typically only available during training and for 3 to 6 months after you finish. So, don’t sleep on this. You should get disability insurance as soon as you have an income as a physician-in-training and fit it into your budget.

Once you have a GSI policy in hand — or you no longer have access to a GSI plan — this is when you apply for a fully underwritten disability insurance policy. The term “fully underwritten” means that it will involve a process where they look into your medical history and may require additional questions or processes to make sure you are someone they are willing to take the risk to insure. Because of this, the fully underwritten process takes longer.

The major benefit is that fully underwritten policies sometimes offer more bells and whistles and the monthly payments are often lower. The major drawback is that with a fully underwritten policy, you can get denied like I did. This risk is unnecessary if you have a GSI policy available to you.

Take Home on Disability Insurance

Getting disability insurance is the number one financial task for a doctor. You can know everything about investing or paying down debt, but without an income none of that matters.

A group disability insurance policy is not sufficient. You need an individual policy. To be clear, if you have any medical history at all (including that one time you saw your PCP for some “test anxiety” or took an antidepressant) you should get a GSI policy. It isn’t worth it to take the risk of applying for a fully underwritten policy unless you know you are completely healthy and have never had a medical problem documented in your chart. If you have a GSI policy in hand when you apply for a fully underwritten policy, it isn’t a big deal. You still get to keep the GSI.

However, you cannot go in the opposite direction. Once you apply for a fully underwritten policy and get denied, you often cannot obtain a GSI plan. That is what happened to me.

Dr. Jimmy Turner is an academic anesthesiologist and the Chief Medical Officer and co-founder of Attend, a comprehensive financial platform built by physicians for physicians. He is also the author of The Physician Philosopher's Guide to Personal Finance and host of the Money Meets Medicine podcast.

Image by Grinbox / Shutterstock